Millions of Americans Are Funding ICE Detention Centers Through Retirement Accounts

A BreakThrough News and More Perfect Union analysis found over $1 billion in retirement-linked funds invested in GEO Group and CoreCivic.

Most people saving for retirement are not choosing to fund ICE detention centers. They are choosing what they have been told to choose: a 401(k), a mutual fund, an ETF, a retirement account, a default investment plan, or whatever option their employer and fund manager make easiest to select.

That is what makes the finding so important. A BreakThrough News and More Perfect Union analysis found more than $1 billion in retirement-linked mutual funds and ETFs invested in GEO Group and CoreCivic, two private prison companies tied to immigration detention. The analysis reported that, as of September 30, 2025, mutual funds and ETFs held about 35 million shares of GEO Group worth roughly $543 million, along with CoreCivic holdings valued at about $472 million.

The issue is not only that GEO Group and CoreCivic profit from detention. The issue is that ICE detention profit can be buried inside ordinary retirement infrastructure, where workers may never see the connection between their paycheck deductions and the companies that benefit from immigrant confinement.

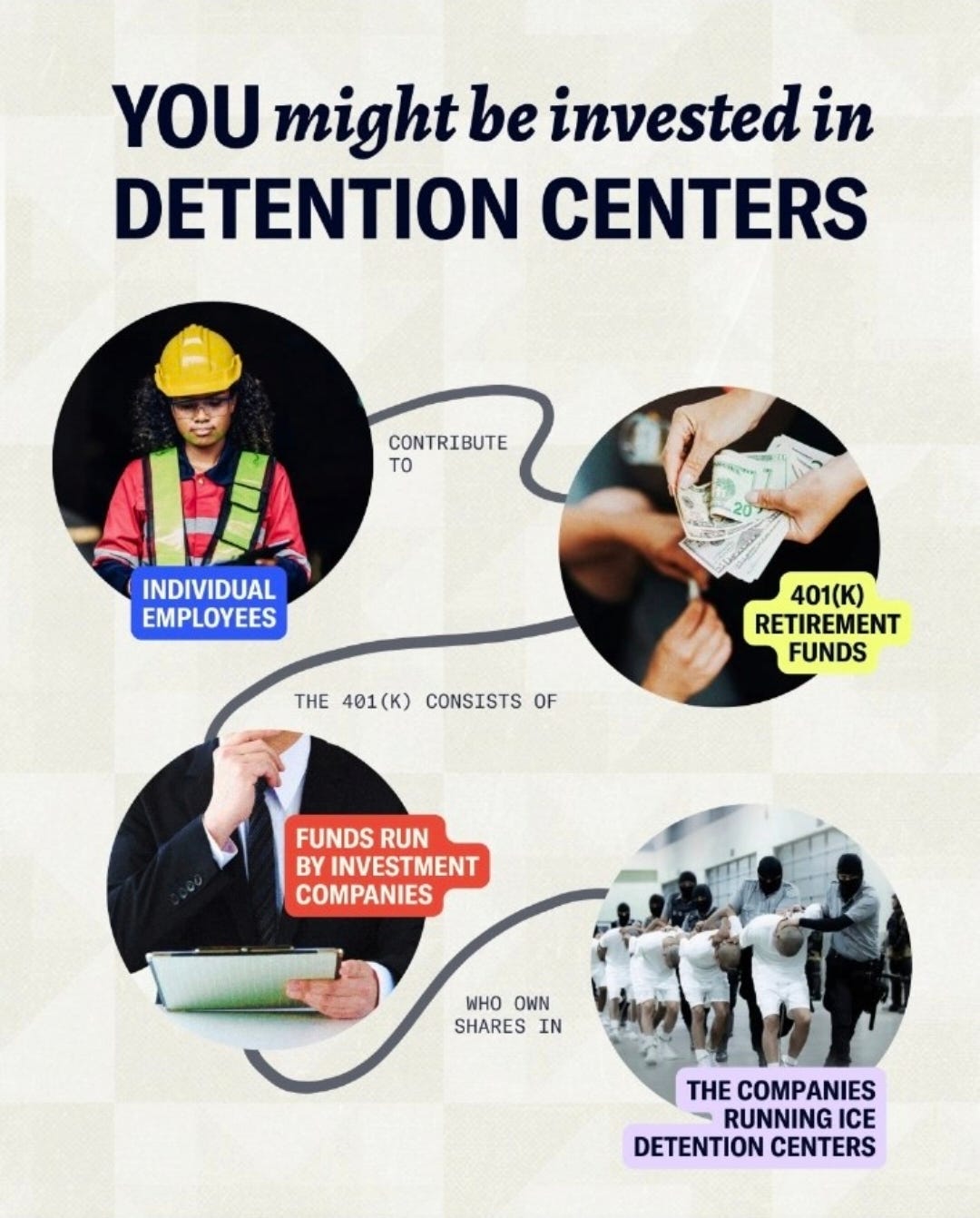

The pathway is simple enough to describe, but easy for ordinary account holders to miss.

A worker contributes to a retirement plan. That plan places money into mutual funds, index funds, or ETFs. Those funds hold baskets of stocks. Inside those baskets can be shares of companies like GEO Group and CoreCivic. The worker may never directly choose GEO Group. They may never directly choose CoreCivic. They may never see ICE detention on a retirement statement. But their money can still flow into companies whose business model depends on incarceration, detention contracts, and the expansion of confinement.

The fund-tracking method matters. Prison Free Funds describes a screening process that examines thousands of mutual funds and ETFs, checks their holdings against companies tied to the prison and border industries, and calculates both dollar exposure and portfolio percentage. The point is not guesswork. The point is that fund holdings can be examined, screened, and traced. When those holdings include private prison operators, the connection between retirement investing and detention profit becomes part of the public record.

BreakThrough’s reporting also identified examples of major investment-firm exposure, including Vanguard-linked GEO Group holdings and Fidelity-managed CoreCivic exposure. Those examples should not be read as a claim that every fund from every firm contains detention-company stock. They show something narrower and more important: some of the most ordinary investment products in the retirement system can carry exposure to companies tied to ICE detention.

That hidden pathway matters because ICE detention does not operate only through uniforms, buses, raids, facilities, deportation flights, and government paperwork. It also operates through contracts, revenue, investors, asset managers, and public markets. The people detained inside immigration facilities are part of one side of the system. The investors who profit from that system are part of the other.

GEO Group and CoreCivic are not passive bystanders in immigration enforcement. They are detention contractors whose business has long been tied to government confinement. When ICE expands detention capacity, when federal immigration enforcement grows, and when detention contracts become more valuable, private prison companies can benefit. That is not an abstraction. It is the financial logic of privatized detention.

The public is often asked to understand ICE violence only at the moment of visible harm: the raid, the arrest, the cell, the deportation, the death in custody, the family separation, the missing person, the mother taken from her child, the worker pulled from a job site, the asylum seeker transferred into a remote facility. But the system does not begin there. Visible enforcement rests on funding, contracts, political permission, and profit structures that make detention expandable.

The BreakThrough News and More Perfect Union analysis pushes that profit trail into the retirement system. It shows how ordinary workers may be financially exposed to ICE detention without clear knowledge, direct consent, or meaningful control over the structure.

The result is a consent problem built into the structure of retirement investing.

A person can oppose ICE detention and still hold a retirement account that indirectly invests in companies tied to detention. A worker can reject family separation and still be placed in a fund that owns detention-company shares. A person can want safety for immigrant communities and still be routed through a financial system that treats private prison stock as just another holding inside a diversified portfolio.

That does not make ordinary workers the architects of ICE detention. It makes them another population whose money can be captured by systems they did not design.

That distinction matters. This article is not blaming workers for saving for retirement. It is naming the machinery that turns ordinary savings into exposure to public harm. Most workers do not have the time, tools, access, or employer-plan freedom to audit every holding inside every fund. Many retirement plans are designed to make passive investing feel neutral, automatic, and frictionless. But passive investing is not morally neutral when the basket includes companies that profit from cages.

Even passive investing can carry active public harm when the holdings include companies that profit from detention.

A fund can passively track an index. An account holder can passively contribute to a retirement plan. An investment manager can passively hold a stock because it is part of a broader market product. But the detention center is not passive. The person locked inside it is not experiencing an index. The family separated by detention is not living inside a portfolio theory. The harm is physical, legal, psychological, and public.

ICE accountability has to extend beyond the agency itself.

It has to follow the private contractors that run detention centers, the companies that profit from confinement, the investment firms that hold their shares, and the retirement systems that can hide those holdings inside ordinary accounts.

Investor-facing materials from detention companies show that this risk is not invisible to the companies themselves. GEO Group and CoreCivic report to investors, file disclosures, and describe business risks in the language of public scrutiny, litigation, government contracts, reputation, human rights, and operations. The companies know that public attention can matter to their business. They know detention is not just a facility issue. It is a revenue issue, a reputational issue, and an investor issue.

BreakThrough reported that GEO Group and CoreCivic did not respond directly to its requests for comment. Instead, the Day 1 Alliance, a trade group representing major private prison contractors, responded by defending services at ICE processing centers and criticizing the report. That response matters because it shows the industry understands this as a fight over public legitimacy, not only portfolio math.

But the average worker may not know any of this.

They may know their employer offers a retirement plan. They may know a percentage of their paycheck goes into it. They may know the name of a target-date fund, an index fund, a large mutual fund, or an ETF. They may not know whether that fund holds GEO Group or CoreCivic. They may not know whether their money is exposed to companies running detention centers. They may not know that the same financial system marketed as retirement security can also help stabilize the profit structure behind immigrant confinement.

That gap is what the reporting makes visible.

The gap is not only informational. It is structural. The retirement system places ordinary people inside investment pathways they do not fully control, then treats the consequences as too technical for public accountability. It allows detention profit to move behind layers: employer plan, fund manager, index provider, ETF, mutual fund, public stock, detention contractor, federal contract, ICE facility.

Each layer creates distance, and that distance makes the system harder to see and harder to challenge.

When detention profit sits inside a retirement account, the harm is harder to see. The investor does not see the cell. The worker does not see the contract. The retiree does not see the transfer bus. The account statement does not show the detained father, the asylum seeker, the child waiting for a parent, the person held in medical distress, or the community living under the threat of raids and disappearance.

The account shows a balance, while the violence behind that balance is made distant enough to deny, technical enough to ignore, and profitable enough to defend.

This is also why the private prison industry’s relationship with ICE deserves public pressure beyond the usual limits of immigration policy coverage. ICE detention is not only a government program. It is a market. It creates demand for beds, guards, transportation, surveillance, construction, food, medical contracts, and facility management. Public money moves into private companies. Private companies report to investors. Investors look for returns. Funds hold shares. Retirement accounts become part of the chain.

The financial chain matters because it shows how detention profit can move through ordinary retirement systems without appearing plainly on an account statement.

The point is not that every person with a 401(k) knowingly funds ICE detention. The point is that the system can make people participants without clear disclosure or meaningful choice. That is an accountability failure. It lets private detention companies benefit from public ignorance. It lets investment managers treat detention exposure as a normal holding. It lets employer retirement plans pass moral risk down to workers who may never be told what they own.

That silence protects the profit structure by keeping workers separated from the detention companies their funds may support.

If a company profits from ICE detention, the public has a right to know who is financing it. If retirement-linked funds hold detention-company shares, workers have a right to know whether their savings are exposed. If investment firms claim neutrality while routing money into companies tied to immigrant confinement, that neutrality deserves scrutiny. If private prison companies warn investors about public backlash, human rights scrutiny, litigation, and reputation, that warning should not stay buried in filings while ordinary account holders remain in the dark.

ICE abuse is not only what happens inside detention centers. It is also what happens around them: the contracts that expand them, the companies that run them, the investors that sustain them, and the financial products that hide them inside ordinary life.

A detention center does not have to appear on a retirement statement for retirement money to reach it. That is the danger. The violence is made distant enough to deny, technical enough to ignore, and profitable enough to defend.

Americans Against ICE tracks ICE harm because enforcement abuse is not only a street-level event. It is an infrastructure. It is raids and custody deaths. It is detention beds and deportation flights. It is contractors and surveillance. It is public money and private revenue. It is also the possibility that millions of Americans are connected to detention profit through accounts they use to prepare for old age.

That connection belongs in the public record.

If ICE detention profit can live inside retirement accounts, then ICE accountability has to follow the money all the way there.

Americans Against ICE documents immigration enforcement abuse, detention profiteering, contractor harm, and the systems that allow ICE violence to disappear into paperwork, contracts, and financial infrastructure.

Upgrade to a paid subscription to support Americans Against ICE and help keep this documentation going.

Outrageous